Talk of recession and stagflation has become a feature of the current investment landscape.

From the lingering effects of Covid to the war in Ukraine and renewed geopolitical shocks in the Middle East, markets have been forced to absorb one wave of uncertainty after another.

The result is an environment where inflation remains stubborn and growth is harder to come by.

That backdrop matters for superannuation investors, but it matters even more for self-managed super fund trustees.

Unlike members of large funds, SMSF trustees are responsible for setting and reviewing their own investment strategy, which means the pressure to stay disciplined in volatile markets falls squarely on them.

Recession or stagflation?

The word “recession” is usually used to describe two consecutive quarters of negative real GDP growth. Australia has not met that definition in decades.

Stagflation is a different beast: weak growth, high inflation and rising unemployment at the same time.

It is especially difficult to manage because the tools used to tame inflation, such as higher interest rates, can also suppress growth and push unemployment higher. That is why markets tend to become more unsettled when stagflation enters the conversation.

The distinction matters because the investment response should not be the same in every downturn. A recession may bring falling prices and softer demand, while stagflation keeps price pressures elevated even as activity slows.

Why Panic Usually Hurts

When markets lurch lower, the instinct to move into cash can be powerful. It feels safe. But history shows that selling after a fall often means locking in losses and missing the rebound that tends to follow.

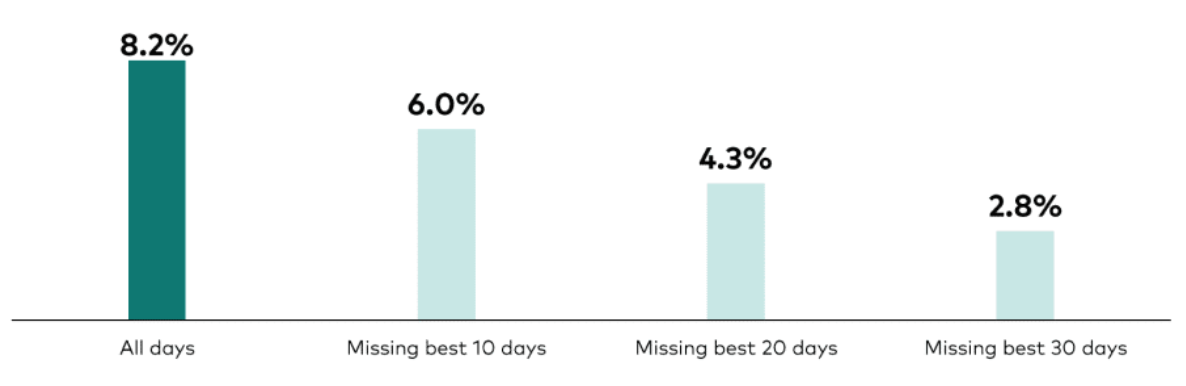

The danger is not just theoretical. Vanguard has shown that missing a handful of the market’s best days can materially reduce long-term returns.

In the chart provided, annualised total return falls from 8.2% for staying invested through all days to 6.0% after missing the best 10 days, 4.3% after missing the best 20, and just 2.8% after missing the best 30.

That is a sharp reminder that timing markets is much harder than staying invested through them.

What the Case Studies Show

The cost of panic is easier to see in real-world style examples.

Carol, 56, had $350,000 in a balanced super option at the end of 2019. When Covid markets slumped in March 2020, she switched to cash and remained there until the end of 2025. Her balance grew to $337,000, but if she had stayed in the diversified balanced option, it would have been $527,000 – a difference of $190,000.

Brian, 67, tells an even starker story. He began with $750,000 in an account-based pension balanced option, switched to cash during the March 2020 sell-off, and finished 2025 with $532,000. Had he stayed invested, his balance would have been $871,000. That meant giving up $339,000 in value.

Unlike members of large super funds, SMSF trustees cannot simply move everything into cash at the press of a button, particularly when the fund holds illiquid assets like property that can take time to sell.

Even so, there is often a temptation to reshuffle liquid, higher-risk assets and build up cash during periods of market stress.

The Vanguard chart below illustrates why that can be costly.

Missing just 10 of the market’s best days cuts the annualised total return on the Australian share market from 8.2% to 6.0%.

Vanguard also notes that the best 30 days account for nearly two-thirds of the market’s long-term return, and those strong days often occur close to the worst ones.

Annualised Total Returns of the Australian Stock Market 2000 – 2025

Source: Vanguard

How to Position a SMSF

For trustees, the answer is not to sit still and hope for the best.

A downturn is a good time to check whether the fund is still fit for purpose and whether the strategy still matches the member’s stage of life, cash needs and tolerance for risk.

A sensible first step is to review asset allocation.

Trustees approaching retirement should think carefully about sequencing risk – the danger that a market fall near retirement does lasting damage to future income. Younger members, by contrast, may see a downturn as a chance to accumulate growth assets at lower prices.

It also makes sense to test whether retirement goals are still realistic.

If inflation stays high and growth stays weak, spending assumptions may need to be revised.

For retirees, holding one to two years’ worth of expenses in cash or term deposits can help avoid selling assets at the wrong time.

Diversification remains one of the simplest protections. If your allocation has drifted away from target, rebalance it. And where individual stock picking feels too risky, diversified funds, ETFs and listed investment companies can spread exposure across sectors and themes.

A Steadier Approach

Downturns rarely reward impulsive moves. More often, they reward patience, discipline and a strategy that has been stress-tested before the pressure arrives.

For SMSF trustees, the goal is not to predict the next shock. It is to make sure the fund can absorb it without forcing poor decisions. In uncertain markets, that is often the real edge.

A Practical Mindset

The best response to uncertainty is usually not to do nothing, but also not to overreact.

SMSF trustees should use volatile periods to test whether the strategy, liquidity position and retirement plan are still fit for purpose.

In other words, focus on resilience rather than prediction. That is often the difference between a fund that weathers a downturn and one that locks in avoidable losses.

If you need to discuss your SMSF please give us a call on 02 9545 5668.